Have you made a resolution this year to get your credit back on track? Have you wondered how to fix your credit or what is involved in figuring out credit scores? Why are credit scores so different? What you see on Credit Karma and what I get in a mortgage score can be totally different. So what do you need to worry about?

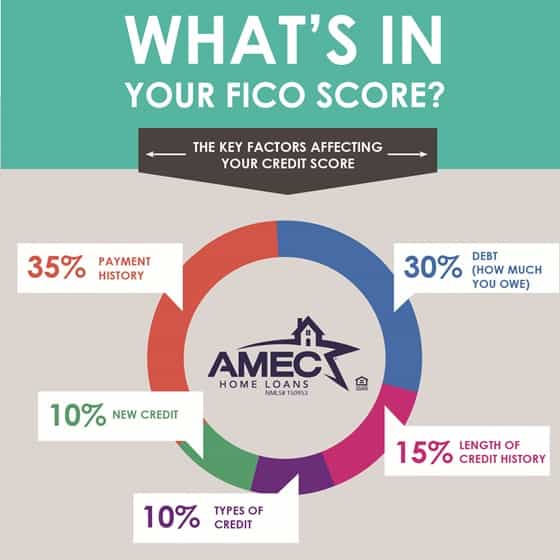

There are five areas of your credit history that make up your score. They are payment history, account balances, the length of your credit history, the types of credit used and how often you apply for new credit. There are two areas that have the greatest impact to your credit score – payment history and account balances.

Your payment history makes up 35 percent of your total score. If you make a payment more than 30 days past the due date, your score will drop. An occasional late payment won’t hurt you too much but continued late payments will definitely hurt. Especially if you reach the 60-90+ day lates. Preventing late payments is very important to your score. I had a client recently that had a late payment, her score dropped over 40 points – as time goes on, it will increase as long as she is on time with her payments.

The account balances compared with the available credit make up 30 percent of your score. This means if you have a credit card with a $10,000 limit and you have a balance of $8000, it will hurt your score. Ideally you want to keep your account balance at about 30% of the available credit. So your score will be much higher if your balance was only $3000 instead of $8000. One of the fastest ways to increase your credit score is to pay down any credit card balances that are over 30% of the available credit.

The remaining areas don’t affect your score very much. How long you have had credit accounts helps your score. Try to avoid closing accounts that you have had for several years. If you have accounts that have been open for years and close them, it can lower your score. The type of credit and number of inquiries both make up about 10 percent of your score. If you have a lot of inquiries, it can lower your score – especially if they are for credit cards. If you are comparing mortgage lenders, pulling credit reports within 14 days of the initial pull should not affect your score.

The best way to improve your credit score is to make sure your payments are on time and that you keep your credit cards below 30% of the available credit. Paying down your credit cards will definitely improve your credit score. Ideally you want 3-4 open trade lines to give you an accurate score. Make sure you are using your credit cards also- you don’t need to use them every month, but you do want to show some activity. Use your cards to pay for gas or groceries and then pay off the balance to avoid interest if possible. Once your score has improved, make sure you keep all your payments on time.

Leslie Vanderwerf, NMLS ID#335509, AMEC Home Loans, An Equal Housing Lender, NMLS#150953 – Email – Website