Although real estate activity slowed down somewhat in June 2024 average sale price held steady with June 2024 at 100.1% and tied with May 2023. Competition sale prices peaked in May in 2022 at 104.1%… in June 2023 at 101.3%… and had a double peak in May and June 2024 at 100.1%.

Competition sale prices over list price held strong in spite of fewer listings closing with multiple offers. There may be 4 offers instead of 14, but the competition is still there when there are multiple offers. According to what I could track from listings that indicated ‘multiple’ offers in comments, 16% of listings that closed in June 2024 had multiple offers, compared with 20.6% in 2023… 21.6% in 2022… and 23.2% in June 2021. That is still higher than 12.8% in the more ‘normal’ market in 2019.

New listings, pending sales and closed sales in June 2024 all declined compared to the last four years.

Months supply of inventory has been increasing every month year-over-year for the last 12 months, but the increase in June 2024 was the lowest since April 2022. Nevertheless, it is nice to see the little humps going up instead of down. The red line on the chart below indicates a balanced market… which shows we aren’t there yet.

Days on the market before pending increased as the % above list price received declined modestly… driving median sales price up to the highest on record.

The percent change in year-over-year median home sales prices was up 1.8% in June 2024, higher than last year but the lowest increase so far this year.

Looking at months supply of inventory by price range shows an increase in most price ranges. The only price range higher than the 5-6 month supply needed for a balanced market is the price range over $1,000,000, with a 6.9 month supply indicating a weak buyer’s market. The lowest supply is in the $250k-$350k price range. Single family homes and townhomes remain tied at a 2.3 month supply. Buyers can be happy with an increased supply of condos for sale… now with 4.0 months supply.

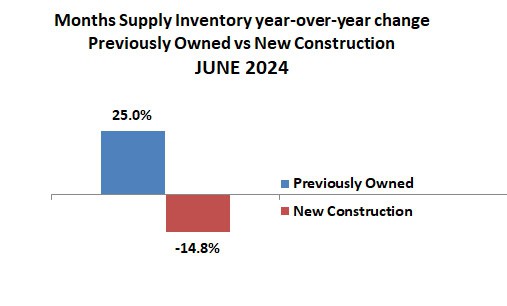

The supply of previously owned homes is up 25% while the supply of new construction is down 14.8% as builders still struggle to keep up with demand.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ area communities

Sharlene Hensrud, RE/MAX Results – shensrud@homesmsp.com

RELATED POSTS