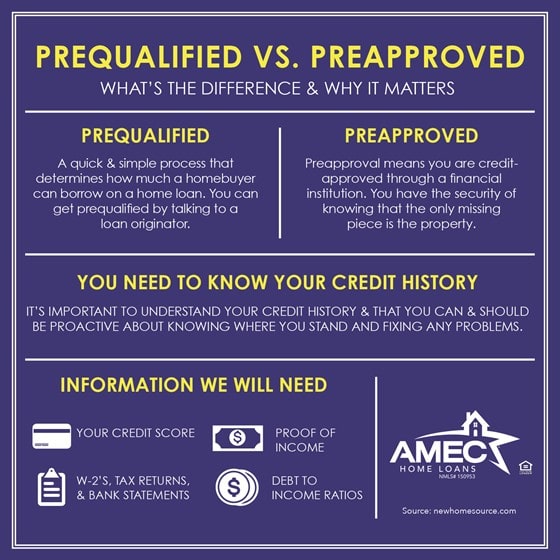

What’s the difference? A pre-qualification means you have talked to a loan officer and they have told you what you might be approved for based on your conversation. There wasn’t a credit report pulled, you didn’t provide income documentation and it truly doesn’t mean much! A pre-approval means you have talked to your loan officer, but you have also provided income and asset documentation, they pulled a credit report and have run your file through an automated underwriting system.

When you are ready to purchase a home, you will want to talk to a lender and get a mortgage pre-approval. With the current housing market, most homes are going quickly and many have multiple offers. When your realtor presents your offer to the listing agent, you want a solid approval so that the seller knows you are going to be able to purchase the home. One option we offer is an AMEC Express Approval. This gives the buyer a closing guarantee and helps the seller to know you will be able to buy. There is a $10,000 guarantee that goes with the AMEC Express Approval – that can make the difference in getting your offer accepted over another offer. This program is available on many of our programs- most conventional, FHA and VA loans. It means your file has been reviewed by an underwriter and not just a loan officer and an automated underwriting system.

Your mortgage approval is usually good for 120 days. Your credit report will expire at that point and you will need a new credit report pulled. Make sure you keep your credit up – no late payments, no inquiries, no new debt – so that your score won’t drop. If you are working on improving your credit, keep track of the payments you have made and if your score is improving. I have clients use Credit Karma and other applications to review their credit. That way I’m not pulling a new report and affecting their credit score.

Make sure your loan officer has your current income information – w2’s, paystubs and tax returns if needed. If you have a raise coming, make sure your loan officer is aware of that. It may make it easier for you to qualify for the home you want.

Once you have your mortgage approval, you are ready to go! Have fun shopping for your new home! Keep in touch with your loan officer and make sure you get any questions answered! Rates are great, it’s a great time to buy a home!

Leslie Vanderwerf, NMLS ID#335509, AMEC Home Loans, An Equal Housing Lender, NMLS#150953 – Email – Website