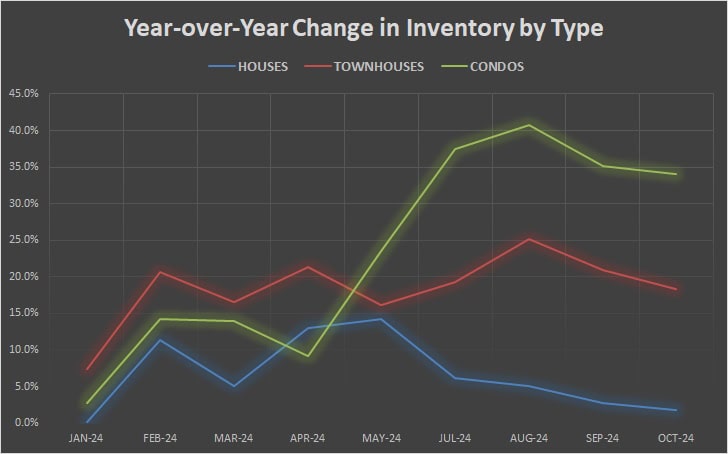

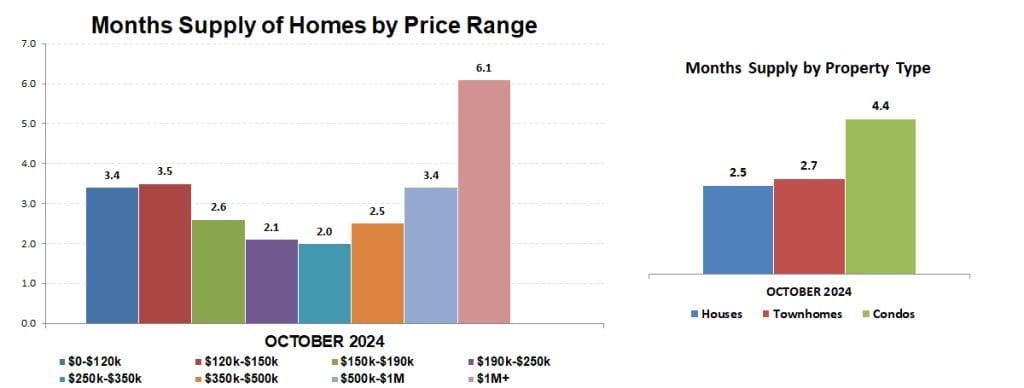

Overall nationwide inventory increased by 23% in October, to a 4.3 months supply. In the Twin Cities metro area overall inventory also increased, but only by 4.0% to a 2.6 months supply. But as you can see in the chart above, condo inventory is increasing at a faster rate than houses and townhouses… with a 41.9% increase over last October, to a 4.4 month supply.

Breaking out months supply by price, all price ranges under $1,000,000 have less than a 4 month supply. The market is considered balanced when there is a 5-6 month supply, so even homes over $1M are close to a market balanced between buyer and seller.

New listings and pending sales both increased compared to last October, by 12.4% and 14.3%. After two months of almost 10% declining sales, October closed sales showed an increase of 5.2% over last year.

Days on market before pending increased by 21.6%, to 45 days. It follows that percent of list price received continues to drop, but only by 0.7%, to average sale price at 97.8% of list price.

Median sales price increased 4.1%, to $380,000 (same as last month)… enabled by continued multiple offers. Inventory still isn’t keeping up with demand. A trackable 12% of transactions closed with multiple offers indicated in the MLS listing… but I know there are many more multiple offers out there that didn’t call for highest & best in the MLS. Instead of 10+ offers on a property common in 2021, one or two offers is now more common.

Sales prices continue to grow, increasing 4.1% over last year… above the national average increase of 3.0% over October 2023.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ area communities

Sharlene Hensrud, RE/MAX Results – shensrud@homesmsp.com

RELATED POSTS