This is a question I hear a lot these days. Many buyers talk about waiting to buy, thinking interest rates will come down. Others have decided to try and buy now. Here are some thoughts to help you make a decision.

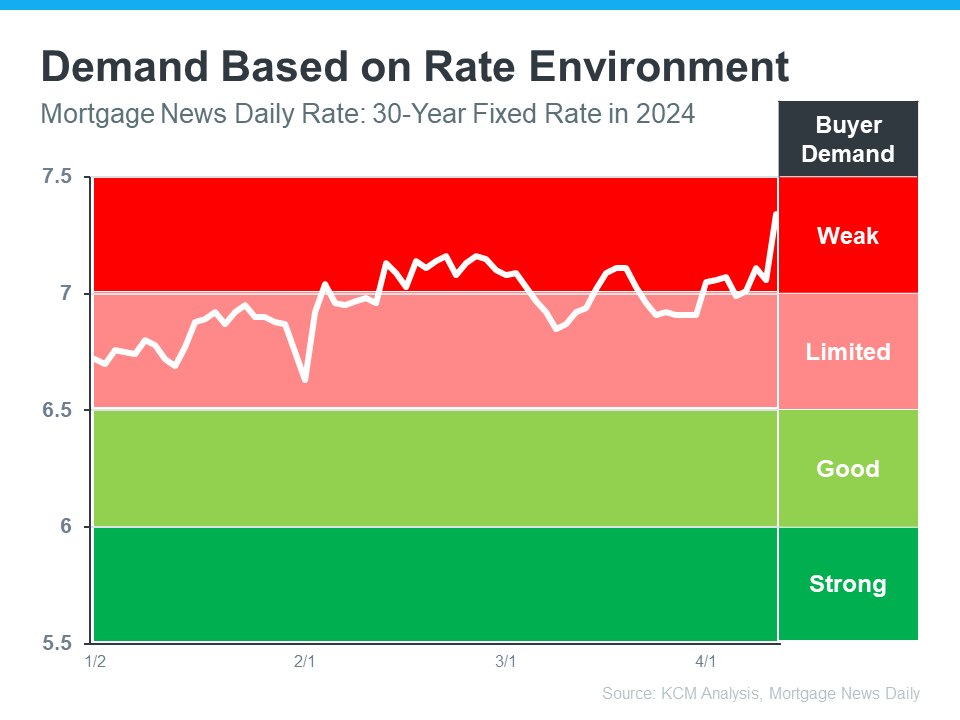

In the housing market, there’s a longstanding relationship between mortgage rates and buyer demand. Typically, the higher rates are, you’ll see lower buyer demand. That’s because some people who want to move will be hesitant to take on a higher mortgage rate for their next home. So, they decide to wait it out and put their plans on hold.

But when rates start to come down, things change. It goes from limited or weak demand to good or strong demand. That’s because a big portion of the buyers who sat on the sidelines when rates were higher are going to jump back in and make their moves happen. The graph below helps give you a visual of how this relationship works and where we are today:

Why You Might Not Want To Wait

If you’re asking yourself: what does this mean for me? Here’s the golden nugget. According to many experts, mortgage rates are still expected to drop some this year, just a bit later than they originally thought. Also rates will not drop as much as originally expected at the beginning of the year. Inflation is still higher than the Fed wants so they are not anticipated to drop rates anytime soon.

When rates come down, more people are going to get back into the market. And that means you’ll have a lot more competition from other buyers when you go to purchase your next home. That may make your move more stressful if you wait because greater demand will lead to an increase in multiple offer scenarios and prices rising faster. We are already seeing multiple offers due to lack of inventory. Add more buyers with lower rates and you will see home prices jump with multiple offers.

Bottom Line

If you’re thinking about whether you should wait for rates to come down before you move, don’t forget to factor in buyer demand. Once rates decline, competition will go up even more. If you want to get ahead of that then look at buying now. A popular saying around here is ” you date the rate, but marry the house”. Remember you can always look at refinancing your home if rates drop.

Part of this blog came from our post at Keeping Current Matters.

Leslie Vanderwerf, NMLS ID#335509, CrossCountry Mortgage LLC, An Equal Housing Lender, NMLS#3029 – Email – Website