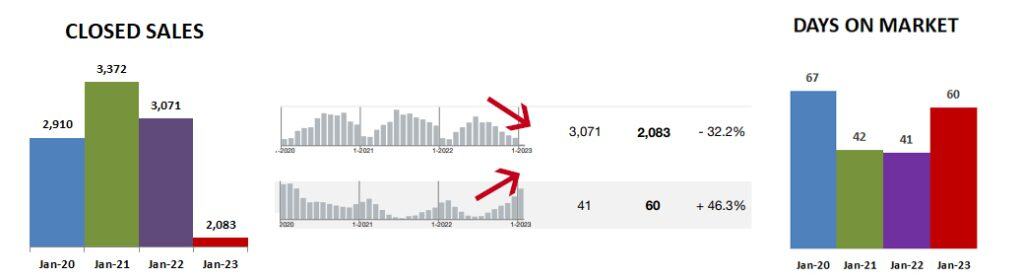

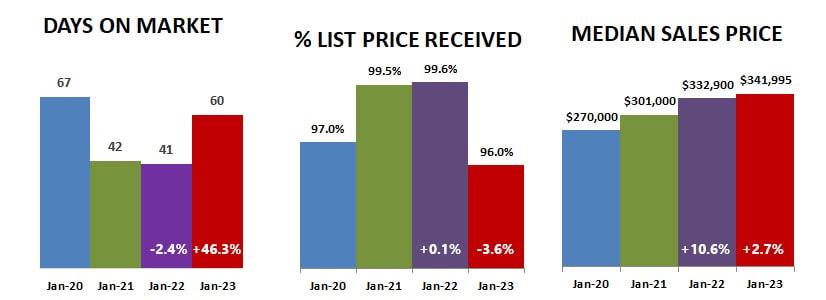

It is very evident from the long term graph above that sales have been steadily falling and days on market have been steadily rising the last half of 2022 into January 2023.

New listings are falling but not at the dramatic rate that pending and closed sales are falling. There isn’t enough inventory to keep up with demand.

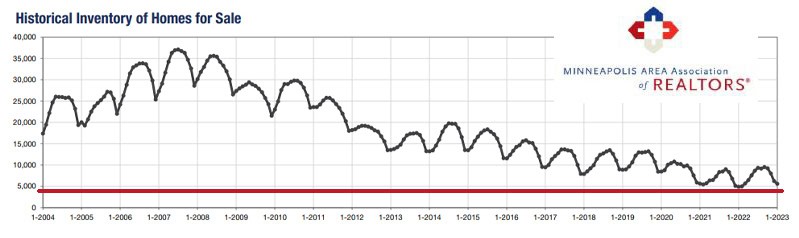

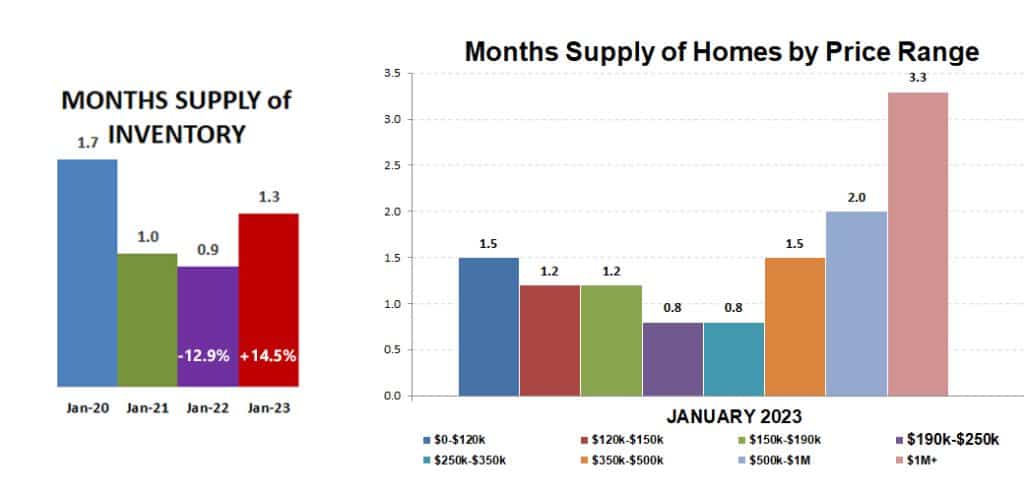

The low sales mean that the supply of inventory is finally going up a bit instead of continually falling. The number of homes for sale in January 2023 was actually 14.5% ahead of January 2022, which appears to have been the lowest point for now.

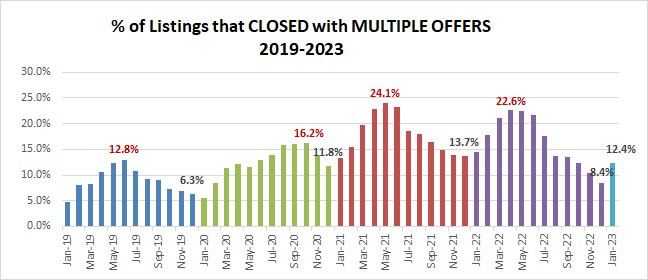

As the days on market before pending increased, the percent of list price received decreased. Median sales price still increased because of competition for limited inventory, but the increase was much lower. As competition for the limited listings increased, multiple offers also increased. In December 2022, only 8.4% of MLS listings indicated there were multiple offers. In January 2023 that percent increased to 12.4%. There may not have been as many offers competing as in the last two years, but there was still competition.

It is nice to see months supply of inventory (how long it would take for the current homes on the market to be sold out if no new listings came on the market) increase compared to last year. The supply is still very low, however, indicating it is still a seller’s market. The market is considered balanced when there is a 5-6 month supply… we have a long way to go.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ metro area communities

Sharlene Hensrud, RE/MAX Results – shensrud@homesmsp.com

RELATED POSTS