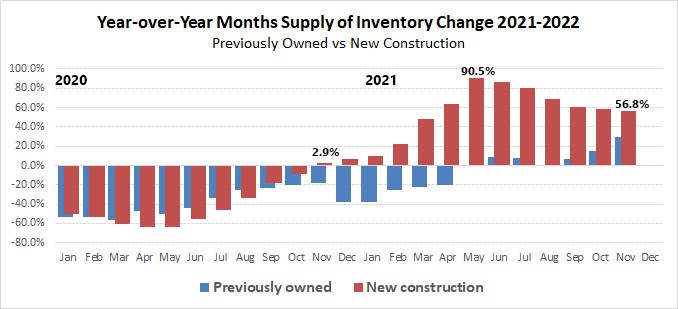

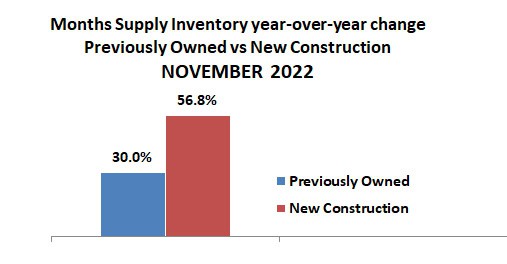

After years of falling inventory with new construction inventory lower than previously owned properties, new construction started to move into positive increases about a year ago. Some of that likely was because of improvements in the supply chain. New construction increased in 2022 to 90.5% over the same month last year in May before starting a gradual seasonal monthly decline which is normal. Months supply of new construction homes was up 56.8% in November 2022 compared to 2.9% in November 2021. Previously owned homes increased by 30% in the same period. Inventory is still low, but it is encouraging to see it increasing.

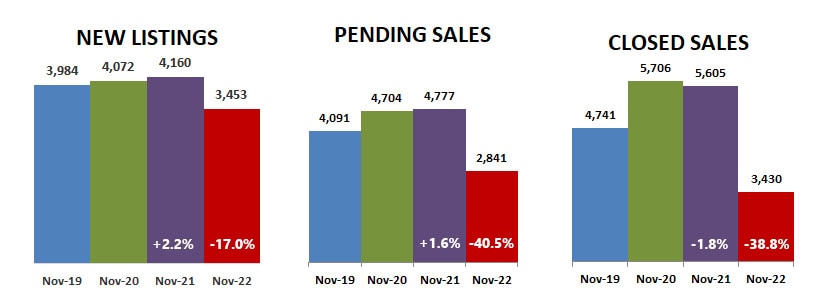

Overall, new listings were 17.0% below last November. Unfortunately, that affected overall inventory which was down more than twice as much. Pending sales were down 40.5% and closed sales were 38.8% below November 2021.

The lagging sales means that the number of homes for sale has increased 12.6% as properties stay on the market longer before pending. But taking into account the declining number of actual sales means the months supply of inventory has increased 41.7%, to 1.7 months.

When you look at it by price and property type, all properties priced under $500,000 had a months supply less than 2 months, and even homes priced over $500,000 still have less than a 5 months supply. That means it is still a buyers market.

Days on market before pending increased to an average of 40 days, up 33.3% over last November. Percent of list price received went down to 97.2%, a decrease of 2.6% compared to November 2021. Median sale price continues to increase modestly, up 4.1% to $354,000.

Percent of listings that closed with documented multiple offers rose from a high of 12.8% in 2019 to 16.2% in 2020 to a high of 24.1% in 2021. 2022 started strong and rose to 22.6% of listings in April and May before falling to 10.3% in November as mortgage interest rates increased. That is still higher than the more ‘normal’ year in 2019.

The stiff competition and multiple offers fueled prices to rise 4.1% in November, the lowest it has been in the last two years.

Buyers and sellers got so accustomed to homes selling for over list price that we are going through a whole new adjustment period as some properties sell for lower than list price, inspections are back in play, and even seller contributions to buyer closing costs are coming back.

Median sale price for November 2022 was $354,000, a little more than 3% below average asking price instead of above, which can bring a ray of hope to buyers.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ metro area communities

Sharlene Hensrud, RE/MAX Results – shensrud@homesmsp.com

RELATED POSTS