The 2018 Twin Cities housing market was marked by low inventory, bidding wars and rising prices. Although prices continued to rise throughout the year, the last half of the year showed a gradual increase in new listings… potentially bringing some relief to buyers in 2019.

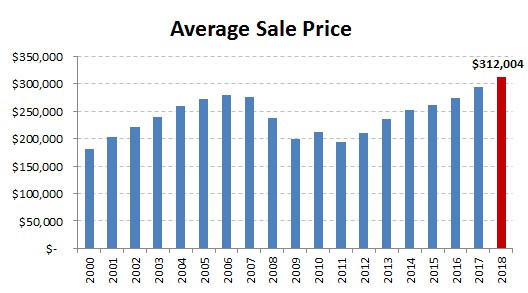

Average Twin Cities sale prices rose 6.3% in 2018 to $312,004, while median sale price rose 7.7% to $265,000. This was the seventh consecutive year of price growth from the low point in 2011, with a 61.4% increase in average sale price and a 76.6% increase in median sale price over that 7-year period.

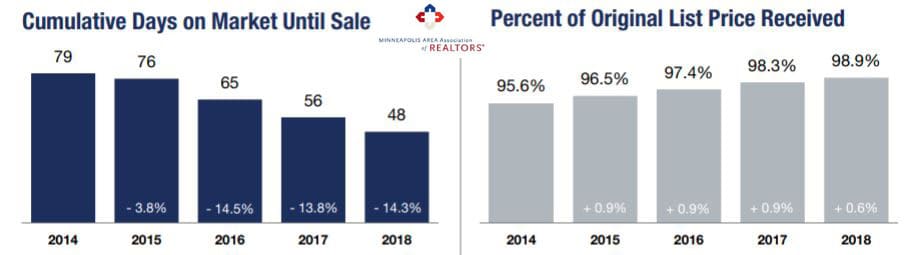

This growth was fueled by a shortage of inventory resulting in bidding wars driving up prices, diminishing days on the market until sale and increased percent of list price received.

Home sales closed in May and June even showed percent of list price received over 100%… likely due to bidding wars in busy March and April.

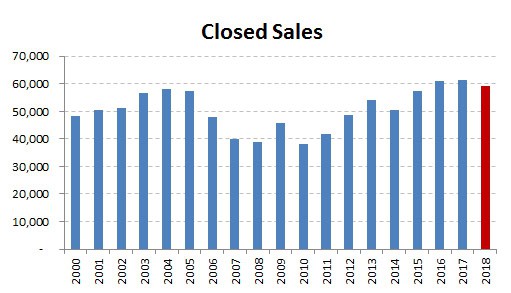

The first half of the year was marked by buyer frenzy, which slowed in the last part of the year resulting in a 3.4% decrease in annual closed sales. A shortage of homes for sale coupled with affordability at a 10-year low made it tough for buyers in 2018.

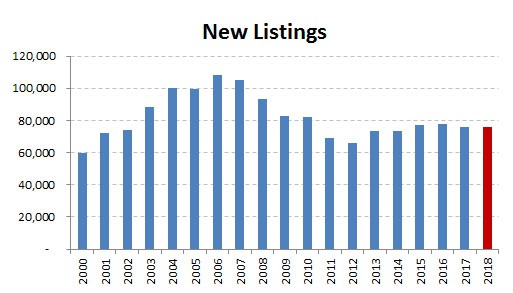

In spite of an increase in new listings in each of the last six months of 2018 the year closed out with the total new listings for the year just 190 below 2017. Expect new listings to show annual growth in 2019.

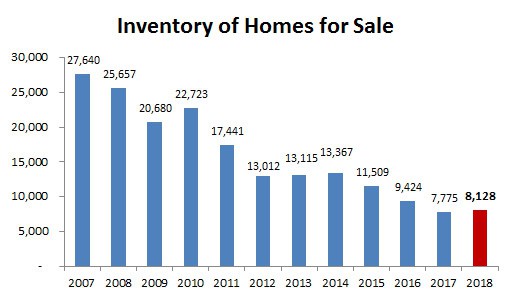

The increase in listings the last half of the year coupled with a decrease in sales resulted in a 4.5% increase in the total number of homes for sale at the end of 2018… a welcome change following three consecutive years of significant falling inventory!

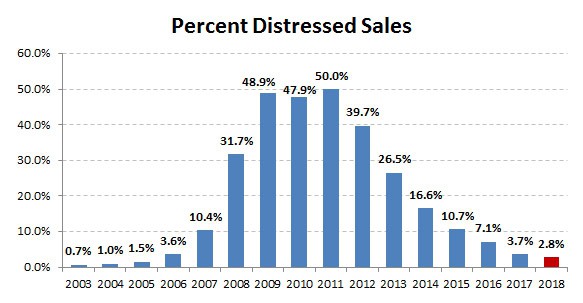

Distressed sales dropped again, to the lowest levels since 2006. This also had an effect on prices and inventory.

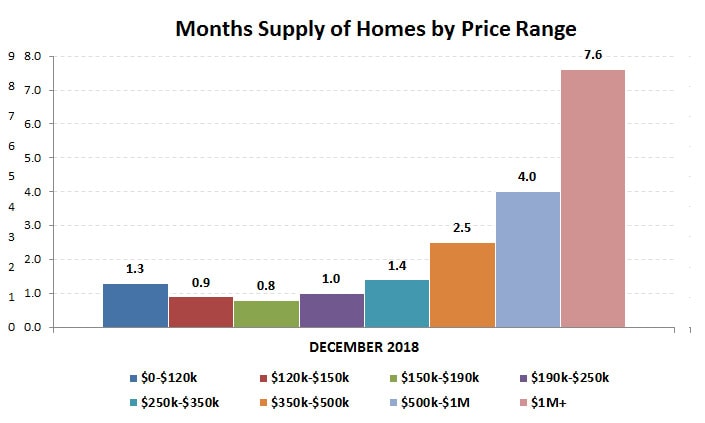

I have long felt the best indicator of the state of the market is months supply of inventory because that takes into account both supply and demand. The market is considered balanced when there is a 5-6 month supply of homes for sale.

The supply varies by price range, but it remains a seller’s market in all price ranges under $1,000,000.

The supply also varies depending on what kind of home you are looking at. New construction had a six-month supply (balanced market) at the end of 2018, while previously owned homes had only a 1.2 month supply (seller’s market). The supply of both increased over last year.

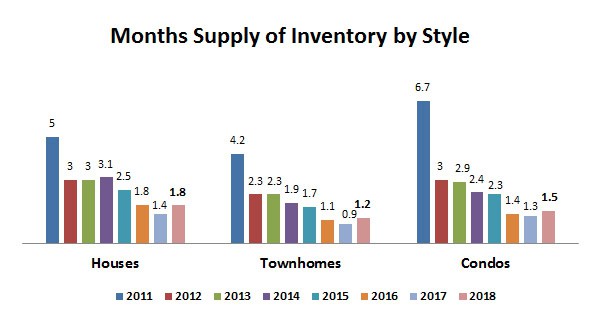

Supply also varies based on property style. Single family houses had the biggest supply at 1.8 months… condos next at 1.5 months… and townhomes with the shortest supply at only 1.2 months. It provides an interesting contrast to 2011, when the supply of condos was approaching seven months!

It can also be helpful to associate prices with different styles and types. It is interesting that new construction condos had the highest median sale prices.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ metro area communities

Sharlene Hensrud, RE/MAX Results – shensrud@homesmsp.com

RELATED POSTS

- December 2018 real estate market update… new trend of increasing inventory

- 7 reasons why now is the time to buy… the biggest challenge for home buyers in 2019

- Listings are increasing over last year… is this a good or a bad sign?

- Softening home prices, falling home prices… what’s happening in the real estate market?

- Homes still more affordable than 1985-2000

- Is another Recession coming in 2020? Another housing crisis?