Last month average sale price was higher than list price for the first time on record. This month it is even a little higher, at 100.3%. Keep in mind this is the average so not every property sells for a price higher than list price… but consider yourself lucky in this market if you are not in a multiple bid situation.

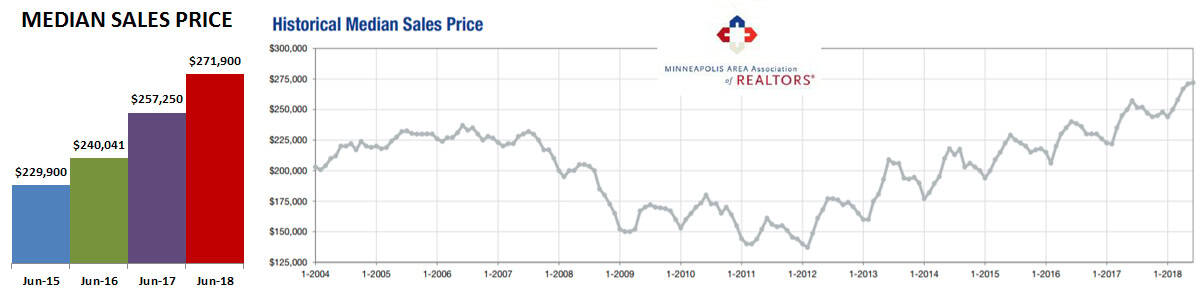

With average sale prices higher than list price it comes as no surprise that median sale prices also continue to rise, although slowing down a bit. Average median sale price for June 2018 was 5.7%, the lowest increase in the last 11 months.

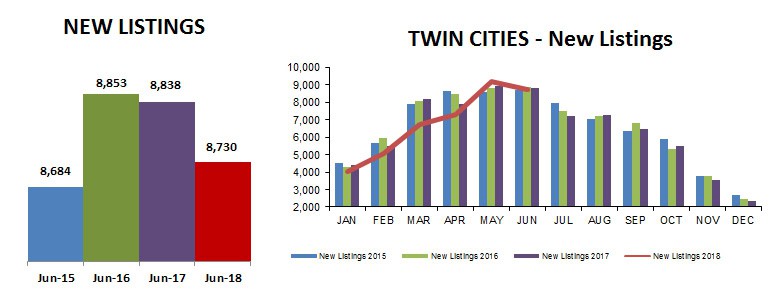

After a nice increase last month, new listings settled back to close to the same as the last few years, to only 1.2% below last year. It looks like the natural seasonal decline may have started a month early this year.

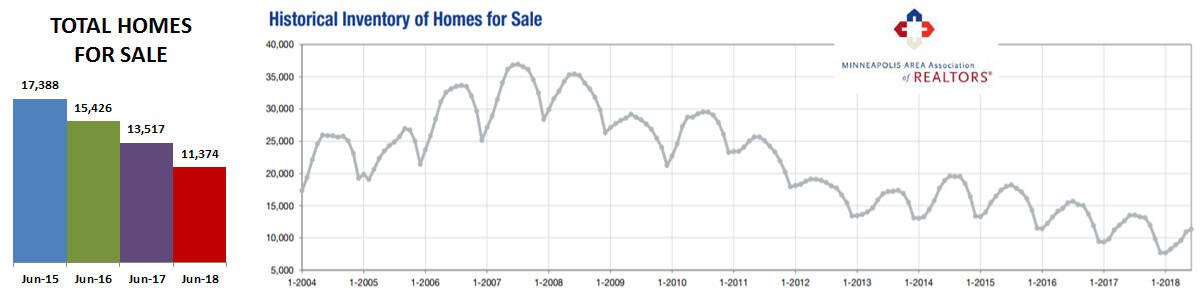

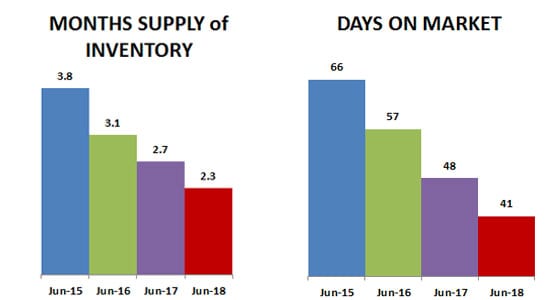

Overall inventory for June 2018 was down 15.9% compared to last June. As you can see by the humps in the chart below, it has been dropping steadily each year since 2014.

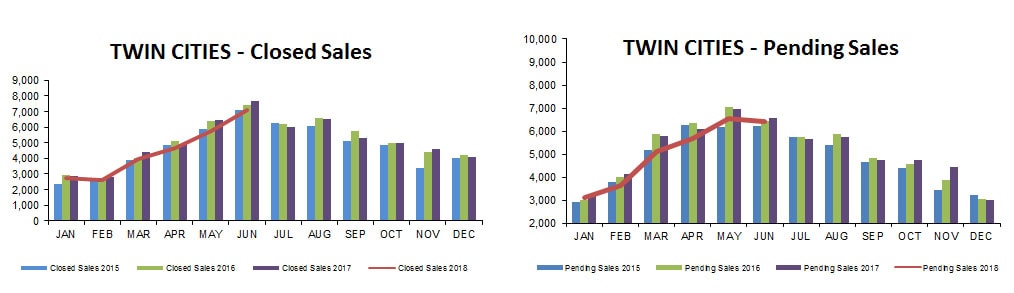

Closed sales continued their climb to the traditional June peak, although 8.1% below last year. Pending sales predict the start of the normal yearly sales arch downward. June 2018 pending sales were 2.1% below last year.

Average days on market before pending was 14.6% below last June and the shortest it has been all year, at 41 days. Although months supply of inventory was slightly higher than last month, at 2.3 months June 2018 was still 14.8% behind last June. The market is considered balance between buyer and seller when there is a 5-6 month supply of homes for sale. We are still in a strong seller’s market.

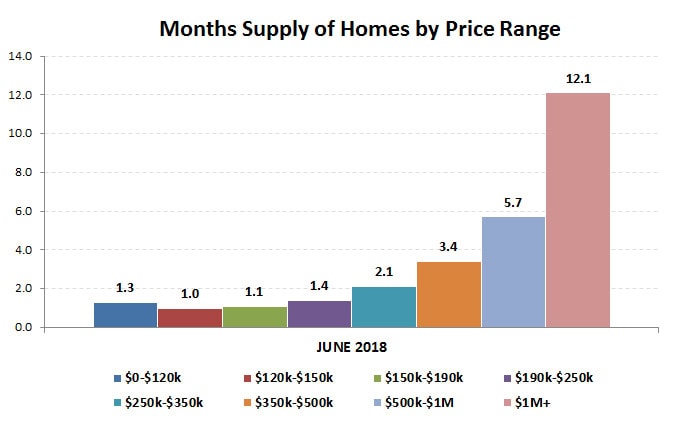

Months supply of homes for sale continues to be lowest for price ranges under $250k, with prices $250k-$350k not far behind with a 2.1 month supply. It is a seller’s market even in the $350k-$500k price range with a 3.4 month supply. Only in the $500k-$1M price is the market balanced between buyer and seller, with fewer new construction homes available than previously existing homes.

Townhomes have consistently been in shortest supply, with June 2018 months supply 20.0% below last year.

The market continues to be strong, with low inventory the biggest challenge. The Fed recently increased the prime interest rate, and while mortgage interest rates are not yet affected buyers may be anxious to buy before they are.

There appears to be slight growth in some new construction, including a shift away from rental units to new developments for purchase.

The figures above are based on statistics for the combined 13-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ metro area communities

RE/MAX Results HomesMSP Team – info@homesmsp.com

RELATED POSTS