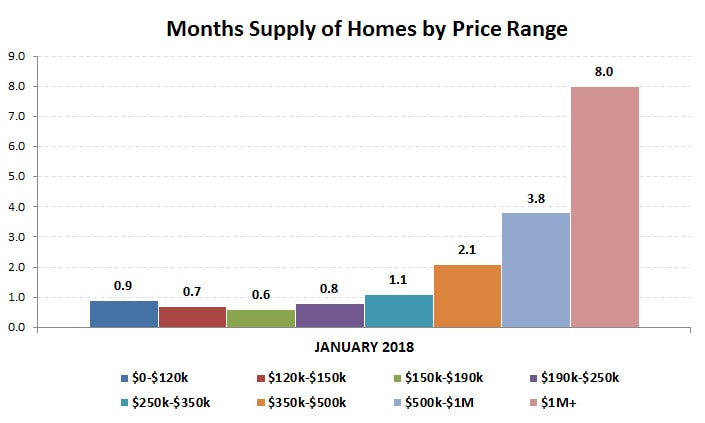

Inventory continues to be the lead story in the real estate market… nothing new! Price ranges under $250k have less than a 1-month supply, but the $250k-$350k price range isn’t much better. With no new listings coming on the market it would take only 1.1 months for those to be gone… and only 2.1 months for homes priced $350k-$500k to be gone. It is even a seller’s market in the $500k-$1M price range… 3.8 months is well below the 5-6 months considered a balanced market. Last January there was a 12 month supply of homes for sale over $1M, this year only an 8 month supply.

Townhomes continue to be the property type in shortest supply, as empty nesters downsize from their houses and first-time homebuyers look for affordable housing stock. These empty nesters may be contributing to the supply shortage, as they seek townhomes when they leave their houses but are unable to find what they are looking for… so they stay put. We attended a seminar yesterday where developers were talking about new townhome developments coming for both first-time homebuyers and empty nesters (something missing in our market for many years)… but they aren’t here yet.

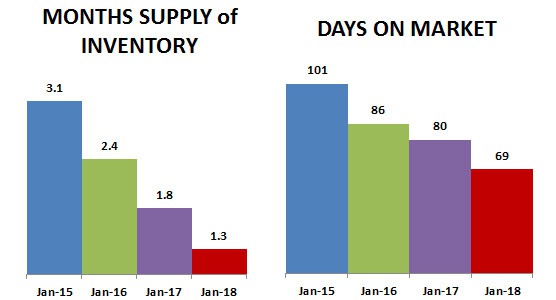

It should come as no surprise that as the months supply of inventory drops so do the days on market before accepting a purchase agreement. Case in point… I listed a property last week and we had two offers the next day!

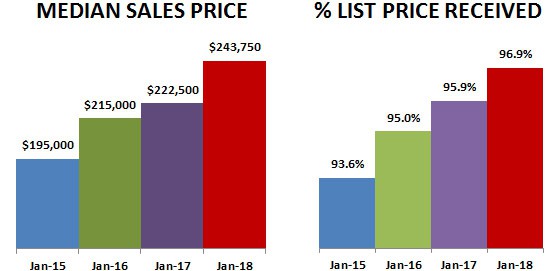

Likewise, prices continue to rise, as does percent of list price received. This isn’t a market where your goal is to see how far below list price you can go. In today’s market you can consider yourself lucky to buy a home without going over list price in multiple offers. Buyers sometimes offer more than list price even without multiple offers to entice sellers to accept their offer before other offers are presented.

New listings in January 2018 were 7.8% below new listings in January 2017. But what is even more significant is the drop of 26.3% in total homes for sale compared to last year.

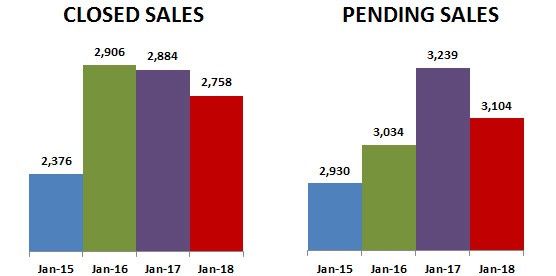

Closed sales and pending sales were both down a little over 4% compared to last year. That is also related to inventory… the number of homes sold is limited by the supply.

Prices that continue to rise have people worried about affordability and another bubble. Looking at the historical affordability index below, the good news is that although affordability is well below the peak in 2012, it is still above its low in 2007 before the last bubble burst. The affordability index for January 2018 in the Twin Cities metropolitan area was 167. That means the median household income was 167% of what is necessary to qualify for the median-priced home under prevailing interest rates.

The figures above are based on statistics for the combined 16-county Twin Cities metropolitan area released by the Minneapolis Area Association of Realtors.

Never forget that all real estate is local and what is happening in your neighborhood may be very different from the overall metro area.

Click here for local reports on 350+ metro area communities

RE/MAX Results HomesMSP Team – info@homesmsp.com

RELATED POSTS

- 2017 Annual Twin Cities Housing Market Review

- Housing predictions for 2018

- So how is the market doing? Weekly real estate market stats