Something I hear a lot these days from potential 'move up' buyers is that they see attractive prices in 'move up' homes but they have to sell first…does it make sense to take a loss on their current home to move up?

Something I hear a lot these days from potential 'move up' buyers is that they see attractive prices in 'move up' homes but they have to sell first…does it make sense to take a loss on their current home to move up?

As with most things in life, the answer really is…it depends…

…it depends on how much equity you have in your current home, which is impacted not only by size, amenities and location but also by your mortgage and home equity credit balances, condition, home improvements, etc

Location can be even more important in establishing value in a down market than a traditional market because some areas have been hit harder by foreclosure prices than others. Ask your Realtor to give you an estimated current sale price of your home and estimated net proceeds after expenses to determine how much cash you may walk away with or need to bring to closing if you sell.

…it depends on what other funds you have available and are willing to invest in a new home. Despite the recent decline in values, most homes still have a higher value than 5 years ago. Real estate is a long term investment, and unlike stocks that can go from peak to zero in a matter of weeks, house values tend to move much slower and you are likely to see growth in its value over time, in spite of down cycles such as we are currently experiencing.

…it depends on interest rates, which can have a big impact on how much home you can afford. Each 1/2 point decrease in interest rate can give you approximately $25,000 more in purchasing power. This means that with 20% down your mortgage principal and interest payment is about the same for a $400,000 property at 6.5% interest as a $500,000 property at 4.5% interest.

…it depends on how you feel about your current home, whether it still fits your needs or you are motivated to make a move.

…it depends on what homes are available for your next purchase…savings are usually greater on a more expensive home so if you are moving up your 'savings' could offset a potential 'loss' on your current home.

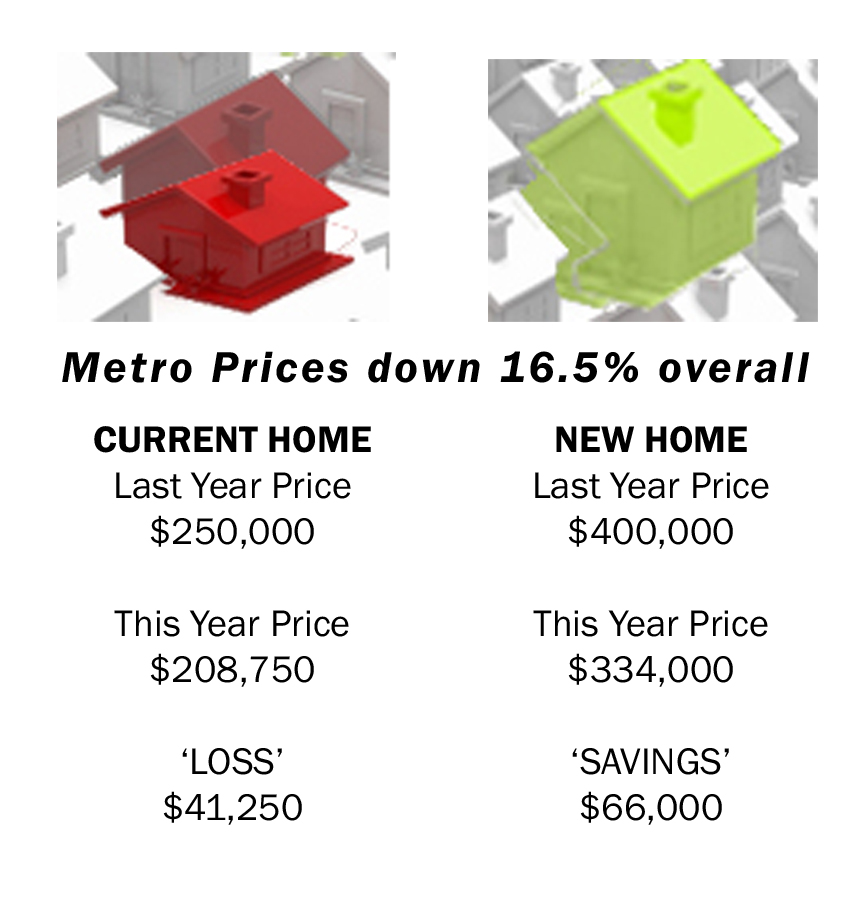

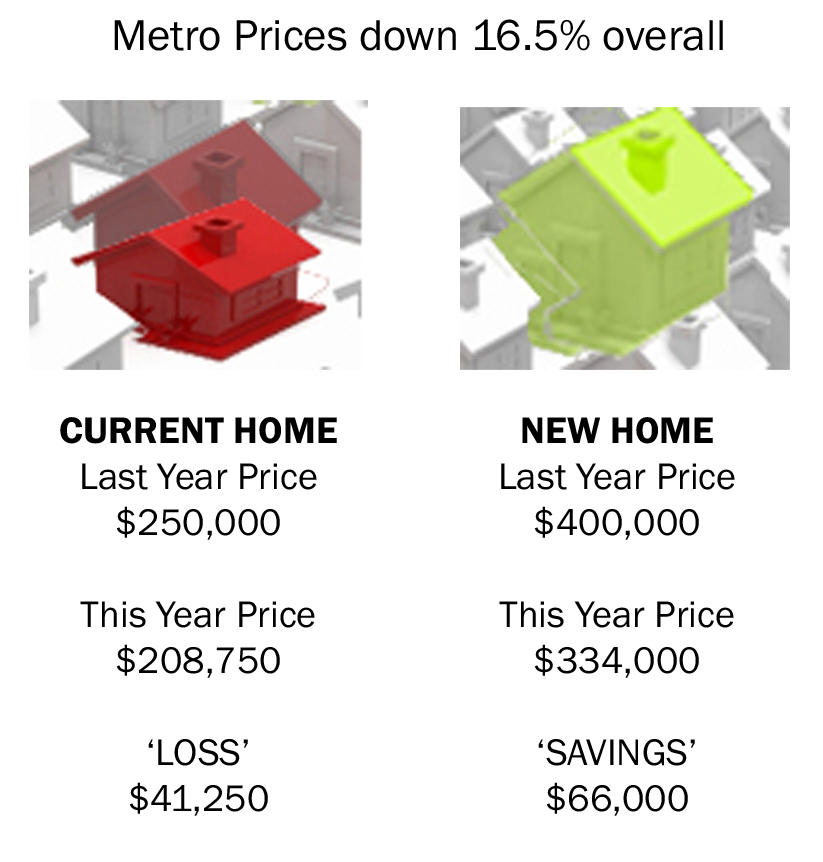

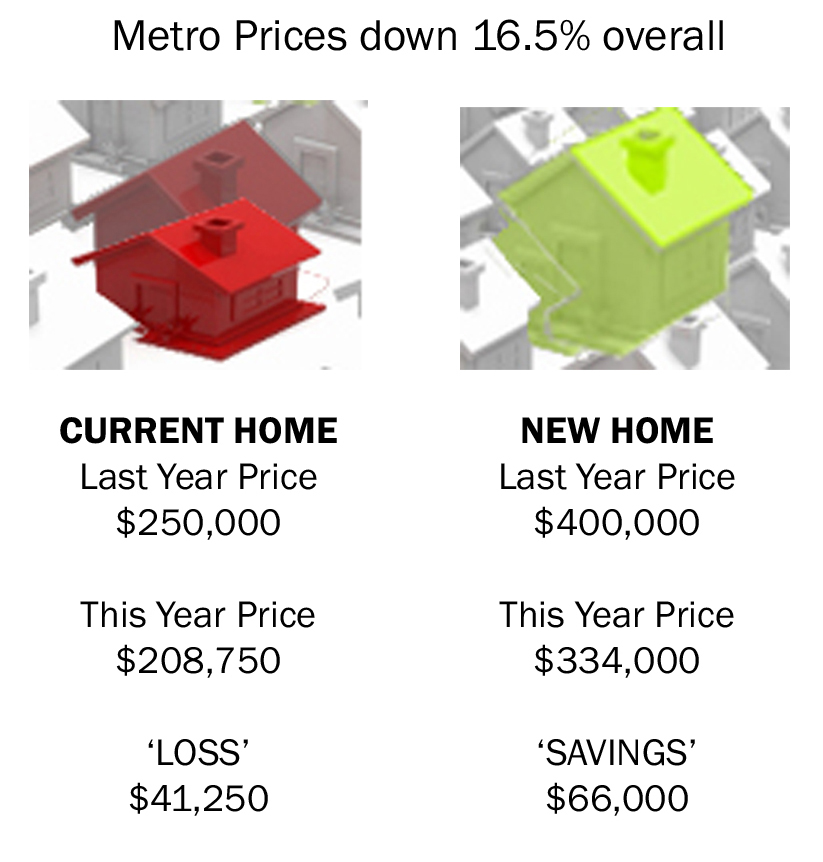

Twin Cities metro area sale prices in October were an average of 16.5% below the same time last year. To the right is an example of how that could translate to a sale and purchase. Of course, this is looking at generalities and can vary greatly depending on the properties and locations involved. Prices have dropped less for properties that are not bank mediated, and sometimes new home savings can be significantly higher, especially on higher priced foreclosure properties. For instance, I just pulled up a Maple Grove foreclosure lake front listing that sold for $885,000 in 2006 and is now listed for $570,000…that's a list price $315,000 below the last sale price!

Twin Cities metro area sale prices in October were an average of 16.5% below the same time last year. To the right is an example of how that could translate to a sale and purchase. Of course, this is looking at generalities and can vary greatly depending on the properties and locations involved. Prices have dropped less for properties that are not bank mediated, and sometimes new home savings can be significantly higher, especially on higher priced foreclosure properties. For instance, I just pulled up a Maple Grove foreclosure lake front listing that sold for $885,000 in 2006 and is now listed for $570,000…that's a list price $315,000 below the last sale price!

The third quarter foreclosure report showed prices were down 9.1% for lender mediated properties but only 4.6% for traditional properties. Assuming that prices have dropped a bit since then I did calculations based on traditional prices being down 5.5% and foreclosure prices down 10.5%…results below.

As you can see from the above, numbers can say different things based on different assumptions…these are simply meant to illustratrate some possibilities based on metro area averages and are based on sale price only, they do not include sales costs. If you are considering making a move, talk to your Realtor to get some realistic numbers for your unique situation, including an estimated net sheet with estimated sales expenses. If moving up could make sense for you, start looking at potential 'new' homes and actually visit some properties to see if it still makes sense…again, your Realtor can be of help. You could be surprised either way!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}